401k Max Contribution Limits and Rules Explained

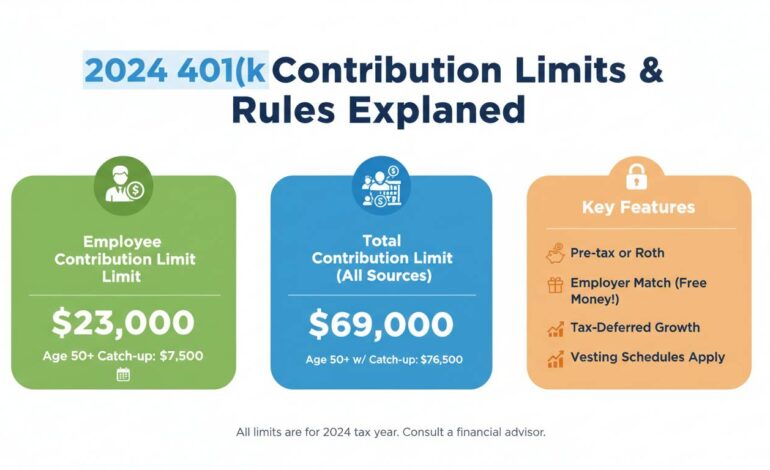

If you’re wondering, “What’s the 401k max contribution for 2024?” — here’s the plain answer: for 2024, the standard elective deferral limit is $23,000. If you’re under 50, that’s your total. Those aged 50 or older can add a $7,500 catch-up, boosting their total to $30,500.

Below is a human-friendly, deep-dive into these limits, context, quirks, and what lies ahead.

2024–2026 Contribution Limits at a Glance

Standard and Catch-Up Limits

- 2024

- Under 50: $23,000

-

Age 50+: + $7,500 catch-up = $30,500 total

-

2025

- Under 50: $23,500

- Age 50–59 (or 64+): + $7,500 catch-up = $31,000 total

-

Age 60–63: + $11,250 “super” catch-up = $34,750 total

-

2026

- Under 50: $24,500

- Age 50–59 (or 64+): + $8,000 catch-up = $32,500 total

- Age 60–63: + $11,250 super catch-up = $35,750 total

Total Annual Additions (Employee + Employer)

This includes your own contributions plus employer matching, profit-sharing, after-tax additions, etc.

- 2024: $69,000 total plus catch-up (if eligible)

- 2025: $70,000 total

- 2026: $72,000 total

Why These Changes Matter (and How to Plan)

Inflation and IRS Adjustments

The IRS adjusts contribution limits based on inflation. That’s why each year brings small increases — like the jump from $23,000 to $23,500 between 2024 and 2025. Gradual but meaningful over time, especially paired with compound growth.

Catch-Up Contributions: Your Golden Boost

Catch-up contributions start at age 50. That’s where many fall short: nearly 85% of eligible workers don’t take advantage of them. If you’re behind, this is your chance to catch up.

Those aged 60–63 get an even bigger boost thanks to the SECURE 2.0 Act—new as of 2025.

SECURE 2.0, Roth Catch-Ups, and High Earners

A big twist comes for high-income savers. The SECURE 2.0 Act has introduced changes starting in 2026.

- If you’re 50+ and your prior-year FICA wages exceeded $145,000, catch-up contributions must be routed to a Roth 401(k) — meaning after-tax entries.

- This applies per employer and is based on prior-year income—meaning new jobs or self-employment may avoid it temporarily.

- Implementation of full Roth requirement has grace: mandatory only from 2027, though high-earning plans can opt in early.

“With SECURE 2.0’s Roth catch-up rule, high-income earners must plan differently. It affects both tax timing and contribution strategy.”

Putting It All Together: A Quick Comparison

| Year | Under 50 | 50–59 / 64+ | 60–63 (“Super”) | Total Additions |

|——–|—————-|——————-|————————|———————-|

| 2024 | $23,000 | +$7,500 → $30,500 | $30,500 | $69,000 |

| 2025 | $23,500 | +$7,500 → $31,000 | +$11,250 → $34,750 | $70,000 |

| 2026 | $24,500 | +$8,000 → $32,500 | +$11,250 → $35,750 | $72,000 |

Real-World Scenario: Jane’s Strategy

Jane’s 62 and making $160,000 in 2025. Here’s how she could plan:

- 2025: Max out $23,500 + $11,250 = $34,750 into her 401(k)

- 2026: Now her income hits the Roth catch-up threshold. She can still contribute $24,500 + $11,250 = $35,750, but those extra contributions must go into Roth.

- Tip: She might front-load or adjust devoted pre-tax vs. Roth strategy. Working with a planner or tax pro helps.

Key Takeaways: Fast and Clear

- 2024 max elective deferral: $23,000; age 50+ adds $7,500 catch-up.

- 2025–2026 bump limits to $23,500/$24,500 elective, plus bigger catch-ups.

- Super catch-up (ages 60–63) emerges in 2025 as $11,250 limit.

- Total plan additions rise gradually: $69K → $70K → $72K.

- SECURE 2.0 forces Roth catch-up for high earners (>$145K) starting 2026 (mandatory by 2027).

Strategic Moves and Best Practices

- Maximize fully: If possible, contribute the maximum. That extra $500–$1,500 a year adds up over decades.

- Use catch-up wisely: Especially if you’re 50+, that’s free tax-saving space.

- Plan for Roth shifts in 2026: If you’re near the income threshold, start talking to your employer or tax advisor now.

- Watch total additions: If your employer offers matching or profit-sharing, you might hit the overall cap before your own contributions max out.

- Track employer changes: Some employers may add Roth options if not already in place—mandatory by 2027.

Conclusion

The 401(k) contribution landscape is shifting steadily. For 2024, your ceiling is $23,000 ($30,500 with catch-up). In 2025 and 2026, both base and catch-up limits climb. There’s a dramatic opportunity for those aged 60–63. And soon, high earners will need to rethink tax strategy with Roth catch-ups. Staying informed—and acting on it—can make a real difference in building a firm foundation for retirement.

FAQs

What is the 401(k) contribution limit for 2024?

The standard elective deferral limit is $23,000. If you’re 50 or older, you can contribute an additional $7,500 in catch-up contributions, bringing your total to $30,500.

How much can someone aged 60–63 contribute in 2025?

They can contribute $23,500 plus an $11,250 “super catch-up,” for a total of $34,750 in 2025.

Are employer matches counted in the contribution limit?

No, employer matching isn’t counted in your elective deferral max, but it does count toward the annual additions cap ($69,000 in 2024, $70,000 in 2025, $72,000 in 2026).

What changes are coming for high earners in 2026?

If your prior-year FICA wages exceed $145,000, your catch-up contributions (for age 50+) must go into a Roth 401(k) instead of pre-tax from 2026 forward.

When do these Roth catch-up rules become mandatory?

Starting in 2026 for high earners, but full implementation (and requirement for all plans) is set for 2027.

Should I start a Roth 401(k) now if I might hit the income threshold?

If you’re close to the threshold or expect additional income, consider setting up or increasing Roth contributions now. Future rules may force catch-ups to Roth, so planning early helps.